This post may contain affiliate links to products that I recommend and I may earn money or products from companies mentioned in this post. Please check out my disclaimer page for more information.

Saving money for retirement does not rank high on bucket lists when you are in your 20’s.

However, imagine being told at a young age in life by a financial planner that

if you can save money, about $1,000 a month, you would be able to accumulate $23.0 million dollars in your life!

That happened to me fifteen years ago.

I was featured in a major metropolitan newspaper for saving money, my extreme money habits, and aggressive retirement planning.

This was before extreme saving and thrifty minimalist living was even a thing.

The newspaper arranged for me to meet with a local financial planner in the area.

They combed through every financial detail of my life and came up with the assumptions that if I took certain steps now, I would be able to retire in my 40’s, live off retirement earnings, and could potentially accumulate $23.0 million dollars.

From that point forward in my life, I was hooked.

Saving Money Retirement Projections

- At age 26, I was saving 11% of my overall salary into my retirement. At that current rate, at age 55, I would have a retirement nest egg worth $970,000. It would be generating $77,000 a year in earnings at 8%.

- By age 70, I would have $2.0 million dollars.

Contributing the Maximum to Retirement Accounts

The financial planner showed me that if I bumped up my contribution and contribute the maximum allowed (which back then was around $13,000 a year), I would have the following amounts in my retirement account:

- At age 46, I would have $1.1 million generating $88,000 in earnings

- At age 55, I would have $2.6 million generating $208,000 in earnings

- At age 70, I would have $7.0 million

- At age 85, I would have $23.0 million

For my current age, I should have a retirement war chest somewhere around $630,000 with earnings somewhere in the $50,000 neighborhood.

I should be on cloud 9 and thinking about essentially planning my retirement; grabbing Kohl’s coupons and looking for plaid pants to chum around Florida in.

Spending my thought time on things like what to have for dinner at 4pm or what activities to do tomorrow after the Today Show is over with should be my focus!

The future never seemed so sweet as it does right now, right?!

What Happened?

Well my friends, simply put, life happened. The predictability of the unpredictable life is what I went through.

One minute you are rocking it in your little caveat slice of world heaven living the Joneses dream life and dropping in at Starbucks daily for your iced latte purchases and breakfast scones.

Blue Heron visit your backyard and pond every morning just as the sun rises to dry the morning dew on your perfectly manicured and weed-free suburban grass cut at the socially-acceptable height with your $2,000 lawn mower.

Yea, crazy right?!

And then one day you wake up and you are trying to keep up with the Joneses next door and make payments on your lawn mower!

Life Changes

Life does not stay constant. The inevitable and unpredictable change happens.

Things that cannot be controlled by you happen and alter your life in various drastic ways that never were a part of your master “life plan.”

I also had two kids who had medical issues; one of which was so severe he would have to go to the ER multiple times a year for something called Cyclic Vomiting Syndrome.

This is a condition that is so severe, if left untreated, it can become life threatening, yet at the same time no one has ever heard of it. Other major changes that were not medical also occurred in my life.

During my decade and a half the following changes happened:

- There was a MAJOR housing crash that lasted over a DECADE

- The stock market crashed

- I suddenly had HUGE mortgages for several houses

- I was forced to become a landlord which was not my life dream

- There were tuition bills for my kids’ private school which was costly

- My family had only one income with a lot of debt that was piling up by the day

- Given all of these financially negative changes that did take place in my life, I had to stop contributing to my retirement and saving money was a thing of the past.

When you are a person who works in finance and deals with budgets and tens of millions of dollars everyday, well let’s just say personal deficit spending is seen as one of the worst financial sins known to man.

My bills were so high that it was a real struggle and challenge to keep everything a float. I could not even afford to contribute 1% into my retirement account because I needed every buck for my current expenses.

Facing Reality

After a long therapy session on my rebar-enforced 700 sqft patio with one of my dogs who clearly was more interested in looking for squirrels and birds then to hear about my financial tsunami troubles (Jack Russell’s are kind of narcissistic like that), I realized I had to start over.

I quickly realized that the answers I wanted about the fate of my future would not come at the snap of a finger.

We live in this society where we demand and, really, we expect instant gratification and immediate answers or responses on our life’s struggles and problems.

Sometimes, however, quick answers don’t work as is the case with personal finance.

We can’t just read a couple tweets, download a spreadsheet and all of a sudden, we are all on the wealth-building path to becoming millionaires.

Examine of Conscious

To move forward on my financial goals, I had to actually go backwards and examine my past financial behavior.

The answers to my financial challenges were in my past and I had to take a step back and sit on the sideline for a bit and examine my conscious.

I decided that, for my situation, I had to first collect data and focus more on these three key points:

- How was I making money

- Where was my money going and what was it being spent on

- How to save money and more of it

I should tell you that this process was not just something I knocked out in a weekend, but it actually took me about 6 solid months to do this exercise.

1. How was I making money?

The first step in my financial data examination was where was my money coming from?

How was I making my bucks? I tracked my income I earned for a couple months so I could have some solid data to look at.

Most of my money, a very large majority of it, was coming from my employer.

There were a few jobs that I did off and on in my spare time between grocery shopping, diaper changing, maintaining my minivan (stow n go…I love you) and running everyone around for doctor appointments that I ended up doing for about 5 years.

Honestly, as I think about it now, I have no clue how I was able to multi-task as much as I did.

One of those jobs was working in Real Estate. I averaged a couple sales a year which I received a commission check from.

This by no means was substantial because the economy at the time was in a MAJOR downturn.

Houses were dirt cheap. You couldn’t really make schwing-bling bucks and bank on selling houses like you can now a days.

But I did learn a TON of information about real estate finance during this period.

Another one was hustling craigslist and selling old stuff or stuff I would pick up stuff off of the street like kids toys.

For this exercise I did not include any of my side hustles and I just focused on my employer income because it was a solid and stable income source I could rely on.

2. Where was my money going and what was it being spent on?

The second step in my financial examination of conscious was to look at where my money was being spent.

This step by far was the hardest step for me to undertake and complete. I knew in the back of my head that yes, I am probably spending way too much money. I did not realize, however, just how much I was spending until I tracked my expenses.

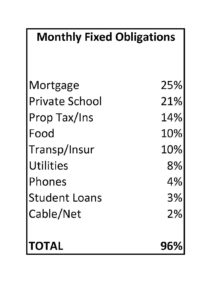

- My top three monthly fixed obligations were my mortgage, private school for my kids, and my property taxes and insurances.

Those three categories were claiming 60% of my monthly pay each month.

That’s right a whopping 60%! Livin’ the dream with manicured lawns, ponds, and blue heron in your backyard is expensive! That was my assessment.

When I looked deeper into the numbers and the expenses, 96% of my monthly pay went to fixed obligations. That was just crazy I remember thinking.

The big shocker was that when I added up ALL my expenses for the month and did a cost per day, the total was almost $200 I was spending a day.

Now, spending $200 a day does not sound like a lot, but when you do the math, it works out to over $70,000 a year.

It was at this life-altering point that I realized I was not in control of my money.

I was stuck in this financial circle of routine bills and monthly expenses that replayed over and over each month and it had been going on for YEARS like this.

My money was controlling my life and yes it was holding me hostage.

I had no savings, no emergency fund, and I was a far cry away from putting anything into my retirement. What was even more alarming was that if I did not make some changes and alter my spending, it could continue on this way for several more years.

3. How to save money and more of it

The third step, I realized I had to make BIG changes if I wanted to be serious about saving money.

I did not want to live this life of debt controlling me and I knew I needed to get back on track with saving money again. My financial position I was in was hard for me to digest, accept, and own because I had a financial background.

Here I was this guy who was featured in a newspaper, who if he saved $1,000 a month, he could potentially accumulate $23.0 million dollars and have the freedom to do anything.

I mean, that’s like winning the lotto basically. And then life threw me some curveballs and I got derailed.

So, I made a commitment to make drastic changes to take back my life and financial freedom.

I looked at various budgeting spreadsheets I had used over the years to manage very large projects in my day-to-day job, along with some personal ones as well.

Then I started to track every buck and cent that I earned and spent and redesigned my financial foundation.

I designed and created a value-based budgeting system that was specifically tailored for me and for every buck that I earned and spent.

I found ways to get back to my foundation of saving money by increasing my income and also reducing my expenses significantly.

If the expense was not a priority in my life, it was eliminated.

Since I was basically saving NO MONEY in my current lifestyle, I had to reduce my expenses.

I made drastic changes such as moving from a $300,000 house that had massive upkeep to a $33,000 place (mortgage-free).

This move changed my views and opinions on a lot of things. Believe me, there were challenges and this was not something that was easy to do.

Sometimes change comes at a cost and sacrifices must be made. The new budget I created definitely reflected that.

And What About That Article?

During the course of this financial examination of my life, I stumbled across the article from 15 years ago, along with some other great treasures such as my AAA safety belt from 5th grade, my collection of micro machines, and some old photographs.

Reading the article did get me back on track with saving money for retirement.

It was just one of those things in life that had I not rediscovered that article at that particular moment in my life, I may not have been as dedicated and forceful to saving money as I currently am.

The article drastically changed the course for me. It was the final push and the final motivation that I needed to make change happen.

Outdated Retirement Analysis

The article itself, however was written over a decade ago so some of the information was not valid anymore.

Back then the maximum a person could contribute to their 401k was $13,000. The new amount today for 2018 is $18,500.

The other major change that happened after that article was written was there is also a second retirement savings account that is now offered that I can contribute to at the same time. The maximum for that is also $18,500.

I felt that with all of these circumstances I had to take action and get back on track with saving money for retirement.

Saving Money Action Plan

With the extra money I had available every month now from my value-based budgeting system I developed and used, I created a saving money action plan for my retirement.

I incorporated three areas into this plan which were to increase my retirement contributions, get all of my retirement statements from the last 18 years, and create savings reports for my retirement so I could track and document the progress from here on out.

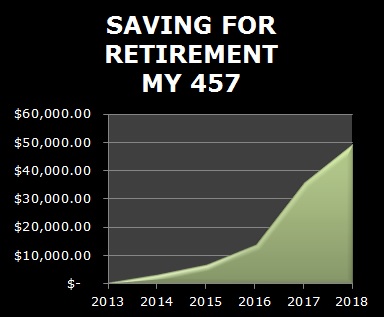

1. Increase Retirement Contributions

The first thing I did with the extra money available was increase my retirement contributions. I had lost a lot of time over the years by not taking advantage of contributing to these pre-tax accounts. So I significantly increased my retirement contributions. This added up to over thousands of dollars per month.

I knew that the information the paper had used to run their projections was different back then. There are new opportunities that exist now. For one, I could contribute a lot more now than back then. I also had a whole second pre-tax account as well now, that was not available to me back then.

During this step, I also wanted to know how much I had contributed thus far in my life towards my retirement. Was I actually ahead at all and have I made any money like the experts claimed I would?

2. My Retirement Statements

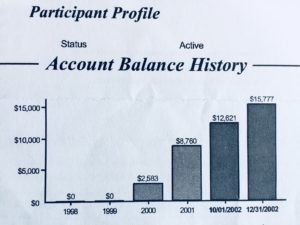

Second, I decided that I needed to get ALL of my retirement statements from almost two decades in order to answer my previous questions.

I went back and gathered as many retirement statements as I could over the course of 18 years because I wanted to see what my YTD had been for each year and if I was actually AHEAD of the 8% gain the paper used or not.

So I called my plan administrator and said

hey I’d like to have all of my YTD statements sent to me because I want to take financial control of my life!

I was shocked when they told me the most they could go back would be only 7 years and I would need a subpoena to go back further?! Crazy, I would need a court order basically to get access to my own financial information.

So I took the 7 years and pieced together what I could find and began to chart everything. Luckily I was able to get most of the data for most years because I had statements tucked away in a shoe box I found in a storage tote.

3. Savings Report for Retirement

The third step in my saving money action plan was to create some type of report where I could quickly analyze how I am doing with saving money for retirement.

It’s important in personal finance and budgeting to go back and look at how you are doing with your goals especially as it relates to saving.

What I learned from this was that even though I had a couple years where I had a MASSIVE loss in value (I lost half of my portfolio value early on), it did come back.

More importantly, I am doing slightly better than just saving the money in a bank account. I am close to the historical 8% return so far for my 401k.

WHAT YOU CAN LEARN FROM MY STORY…

Everyone has a different story in this world. These events happened in my life. I was on a path of saving money for retirement and I got derailed by events in my life and I lost sight of this elementary and fundamental lesson of saving money.

For a decade and a half I lived a life that was extremely stressful financially and incurred lots of debt.

I made debt-driven purchases that in reality only bought me a facade of happiness.

And then one day I decided I didn’t want to live that way anymore and I made a change. I changed my life.

I found ways to make change happen, created new ways to save, made new household budgets, developed savings models, and I am now back on track with saving money again!

My story is as much about having the will, drive, and desire to make the change happen as it is about saving money.

If you want to live a life debt-free and stress-free it is never too late to take action and start saving money.

If you want to make a change in your life, you can do it too. Get involved, learn about your day-to-day finances, and take action.

I will be posting tools to help families, households, and others get back on track with saving and budgeting along with lots of other fun interesting stuff such as how I am making money online too. I invite you to follow my page and look for exciting things to come. It’s Smart Cents!