Knowing how to improve your credit score is as important as knowing how to brush your teeth.

Your credit score is one of the most important numbers in your life. Having acceptable credit is second to knowing personal budgeting methods. It will dictate a lot of things in your life for you.

Some of these things include whether or not you qualify for a mortgage loan, being able to use credit cards, purchase a car, or even qualifying to rent an apartment.

Your credit score is used for so many things even how much you pay for auto insurance and what type of mortgage rates you qualify for.

The number which makes up your credit score is used as a measuring tool. Many establishments use it to determine financial risk to them.

- For example, a bank wanting to give you a loan for a car will look at your credit score number and determine whether or not you are willing to pay each month on that loan or not pay.

The higher the credit score the more likely you are to pay on that loan.

That is why it is essential that you know how to improve your credit score.

But before we can go into those details, we have to look at what your credit score is made up of it how it is determined.

What Makes Up Your Credit Score?

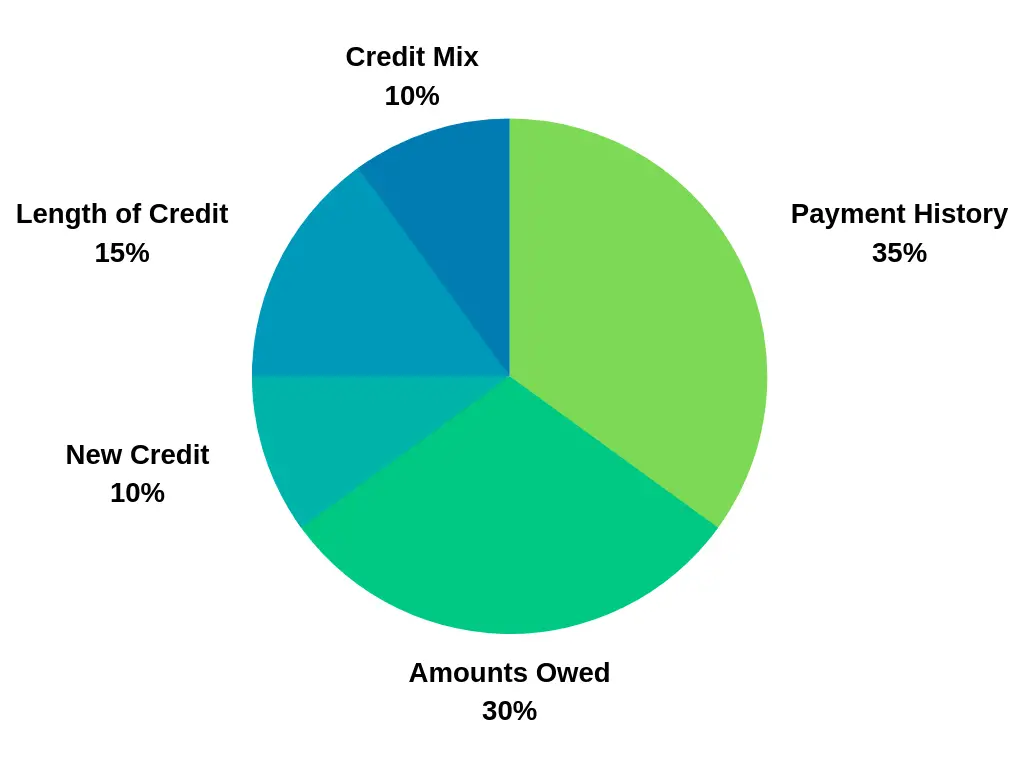

Your credit score is based on several different factors. The number one factor however is payment history. The amounts you owe is the second biggest factor. Those two factors alone make up over 60% of your credit score.

Other factors that affect your credit score are credit utilization, or how you use your credit, length of credit, and new credit lines opened.

Credit Score Basics: What Do Credit Scores Mean?

Credit scores range from 300 to 850. The higher the score the better the credit. A higher score demonstrates good credit history, low credit use, and good on time payments.

Lower scores indicate those borrowers have more risk. Some of those risk factors would include late payments that would be displayed on their credit report or over extended use of credit lines.

The different credit score classifications are explained below:

Exceptional: 800 to 850

Scores ranging from 800 to 850 are considered exceptional. People with scores in this range typically experience easy approval processes when applying for new credit. They are also likely to be offered the best available lending terms, including the lowest interest rates and fees, and are not associated with a lot of lending risk.

Very Good: 740 to 799

Scores in the 740 to 799 range are deemed very good. Individuals with scores in this range may qualify for better interest rates from lenders. They are also associated with a low-borrowing risk to lenders.

Good: 670 to 739

Scores in the range of 670 to 739 are rated good. Most Americans fit into this range. This range includes the average U.S. credit score, and lenders view consumers with scores in this range as “acceptable” borrowers.

People with scores in this range are likely to qualify for a broad array of loans and credit cards but are likely to be charged interest rates somewhat higher than the best available.

These borrowers are considered more riskier than borrowers with very good or exceptional scores.

Fair: 580 to 669

Scores that range from 580 to 669 are considered fair. Lenders may disqualify individuals with these scores if they apply for mainstream loans. Consumers with scores in this range may be considered subprime borrowers. However you can still qualify for car loans.

They may only be eligible for loans with interest rates significantly higher than the best available. There is an increased risk to the lender with a borrower who has a fair credit rating.

Poor: 300 to 579

Scores that range from 300 to 579 are categorized as poor. Many lenders decline credit applications from people with scores in this range, which could be a result of bankruptcy or other major credit problems. Credit applicants with scores in this range may only qualify for secured cards that require placing a cash deposit equal to the card’s spending limit.

In addition, utilities may require customers with scores in this range to put down sizable security deposits. This is due to the fact that these borrowers have serious risk to the lender that they may default on payments.

Credit and Real Estate Financing

In regards to real estate finance, credit scores are also important.

Before you can save money for a house down payment, you have to get your credit score to an acceptable level to qualify for a mortgage.

To give you an idea on qualifying for a mortgage loan, some lenders will approve mortgage applications if the applicant has a score of 680.

When I sold real estate, I had some clients that had scores around this level. The ones that could not qualify for a mortgage, I assisted them with credit repair to get their credit scores up. We will cover those steps later on in this article.

For mortgages to qualify for a great mortgage rates and also for other lenders outside of mortgages, 720 is viewed as the ideal credit score.

Any borrower that has a credit score above that number, they would qualify for the best loan and interest rates available as their credit is in the top tier. A lender loves a borrower who will pay their mortgage regularly or even better if they are able to pay off their mortgage early.

What Can Affect Your Credit Score?

There are all different kinds of scenarios that can affect your credit score number. Some of those factors are included below:

Do you often make late payments on your bills?

As discussed above, payment history is one of the largest factors when determining your credit score. With every late payment, your score will drop. If you do happen to miss a due date, make the payment as soon as possible.

Often times there may be a 30 day window before the late payment is reported to credit agencies

Are your credit cards maxed out with large account balances?

Remember credit utilization is the other major factor that determines your credit score. The amount of total debt versus the total credit limit plays a huge role. Very high balances mean that your credit cards may be maxed out which often displays a sign of poor credit management.

If you had a $5000 credit limit and you are carrying a $4000 balance on it, your credit utilization ratio is 80%. That will affect your credit score.

Are all your credit accounts new?

If you tend to open up a lot of new credit accounts, this will affect your credit score as well. Having open lines of credit available often display that you are able to manage your credit appropriately.

What type of credit do you use?

Diversifying your credit use can also play a role in determining your credit score.

The credit bureaus want to see evidence that you can manage a variety of different credit types.

Some of those would include:

- credit cards

- recurring payments

- private bank loans

- mortgages

Paychecks And Your Credit Score

Before you can improve your credit score, you have to have a solid understanding of where your finances are going.

This is important if you are living paycheck to paycheck.

1. Where Is Your Money Going?

According to a recent CareerBuilder report, 78% of US workers are living paycheck to paycheck.

Understanding where your money is going is an essential part of the process of increasing your credit score.

You have to reduce your expenses if you find yourself short each month. Knowing your monthly expenses and using a personal finance flowchart is the first step to overcome any deficits and overspending that take place each month.

2. End Each Month With Extra Cash

Go through your expenses and determine where you can make adjustments. Maybe instead of eating out a few times a month, you only eat out once a month.

Trimming your expenses is necessary in order to restore fiscal order to your monthly budget if you find yourself over spending. The goal here is to reduce your expenses enough where you finish the month in positive territory with some money left over.

3. Don’t Borrow Money Or Credit

Staying clear of loans and new credit is essential to improving your credit score. Now that you have money left over each month, you can apply that additional money to pay down balances.

I also recommend paying cash as much as possible in this step. Studies show that when people pay cash for items, spending decreases between 10% and 30%.

This is because when people pay cash, it really forces a person to determine if this purchase is a “need” or a “want.”

When you are paying with cash, you only have so much available whereas when you pay with plastic, it’s more unlimited and you may not scrutinize that purchase as much.

4. Focus On Paying Down Debt

Now that you have extra income each month, use that money to pay down debt.

Being able to tackle your debt and credit card bills is essential to increasing your credit score.

If you have student loan debt, try to find ways to pay down those balances.

Once you start chipping away at your debt, eventually your score will improve.

Tips On How To Increase Your Credit Score

Once you have extra income available each month, following the steps below will put you on the fast track to increasing your credit score in no time.

1. Pay Down Maxed Out Credit Cards First

If you have several credit cards that have a balance on them consider paying them off. Take a look at the credit card that has the amount owed closest to the credit limit per card.

You should pay off that one first so you can bring down your credit utilization rate. Think about moving back in with your parents to save money so you can focus on paying off credit cards. By increasing your credit utilization rate your credit score will start to increase.

2. Pay Numerous Times During The Billing Cycle

One of the things I do to help my credit score is pay the amount I charged on the credit card every week. Instead of only making one payment each month, I will make one payment each week for all of the charges I made.

This keeps my credit score high since I’m constantly improving my credit utilization rate.

3. Payment Reminders

If you are not able to pay on your credit cards weekly, then consider setting up payment reminders.

Keep a calendar of all of the payment deadlines for each bill.

Set up notifications to remind you to pay these bills. You can use your phone as well to set notifications which is extremely convenient.

By paying your bills on time and creating a budget, you could improve your credit and your score within in a few months.

4. Applying For New Credit

Be careful for applying for new credit. This could potentially lower your score if you are applying for too much credit in too short of a time period. Learn how to get a credit card without a bank account if you don’t have one.

Only apply for credit when you absolutely need it if you are trying to improve your credit score. Even the application process of applying for new credit dings your credit reports a couple points every time. So be sure you absolutely need the credit before you apply for it.

Even establishing utility bills can help. Determine legally, can you put your electric bill in someone else’s name to improve scores.

5. Contact Your Creditors

If you are having a hard time paying your credit card balances, contact their customer service department.

Explain to them your financial situation and see about setting up an alternative payment plan if you cannot afford your monthly balance.

Although you are still coming up short on the monthly payment, this will reduce the negative affects of late payments or not making the payment at all.

Often times your creditors may also lower the interest rate on your credit card which is also a huge benefit financially.

If you are carrying a credit card balance of $10,000 or more and they agree to lower your interest-rate a few percentage points, you may see a monthly savings of several hundreds of dollars.

By contacting your credit lenders, you may be able to get out of debt sooner instead of later.

6. Keep Unused Credit Card Accounts Open

Credit history is responsible for a large percentage of your credit score. If you have unused credit cards, do not close those accounts.

The longer the history of credit you have, the better your score can be.

You can always get an online store credit card with guaranteed approval for building credit. Always keep unused credit lines open. Additionally, maintaining a low credit utilization ratio by not maxing out your available credit can further boost your credit score over time. If you’re looking to maximize your options, explore some of the best shopping sites with credit lines, as many offer flexible payment options and exclusive deals. Remember, responsible spending and regular, on-time payments are key to maintaining a healthy credit profile.

7. Diversify Your Credit Accounts

The different types of credit you have also have an impact on knowing how to improve your credit score. Your credit lines, secured versus unsecured loans, do play a role on your score as do the types of credit.

Auto loans, credit card payments, and cell phone bills all affect your credit account differently. That is why it is important to keep all different types of credit open. Just be sure to make the payments on time.

8. 0% Interest Credit Cards

While not directly related to improving your credit score, this is a special bonus tip for somebody that already does have good credit.

Think about applying for a 0% interest card also known as a balance transfer. It is smart to do this if you have an auto loan at 6% interest.

I followed this strategy to pay off a $30,000 vehicle that had a 6% interest-rate. Not only did I save a substantial amount in interest, I also ended up keeping the credit card line open once the balance was paid off.

Additionally I was able to pay for the vehicle a lot faster by using a 0% balance transfer card instead of traditional auto loan financing.

But, like I said, you have to have good credit in order to qualify for such an offer.

9. Review Your Credit Report Annually

You should review your credit report every year and look for errors. There are many websites out there that claim to offer free credit reports. I only use annualcreditreport.com because I know it is 100% free to request a copy.

By law, you are allowed one free credit report from each credit reporting company every 12 months.

This is a great free tool how to improve your credit score annually.

Review your credit report closely and if you find any errors be sure to dispute them with the credit agencies. This is a relatively easy way and often a very quick credit fix.

You want to be sure that your credit report is accurate and that there is not any false information on the report.

Especially with identity theft being so common these days, it is even more important that you check your credit report annually.

10. Raise Your Credit Limits

If you are able to control your spending, another good trick to use is to increase your credit card limits. The advantage of this is that you are improving your credit utilization ratio. By requesting an increase in your credit limit, your utilization credit ratio goes down.

Do not do this however if you have missed payments with the particular credit card and question. The credit card company may see this as a sign of financial troubles and that you are having a hard time paying your bills.

Your score could potentially go down as they may see this as you need the extra credit due to some type of financial distress.

For people who have a score in the 630 to 700 range this is a good strategy to use only if you are able to not use the new credit.

What to Look for in a Credit Report

When you have a copy of your credit report there are a couple things that you should pay attention to. Those would include mistakes such as:

- a misspelled name

- wrong Social Security number

- credit accounts belong to someone else with the same name different address

- incorrectly reported late payments

- incorrect delinquencies that are listed twice

- accounts that are closed but still reported as open

- accounts with an incorrect balance or credit limit

What If I Filed For Bankruptcy?

Chapter 7 bankruptcy is on your report for 10 years and Chapter 13 remains for seven years.

Bankruptcy will definitely impact your credit score. The bankruptcy and/or defaulting on a mortgage will stay on your credit report for seven years.

During the housing crisis a lot of people had foreclosures on their credit reports. Some of them however, were able to work out deals with their lender and sold houses on a short sale.

You can also get ahead by implementing household budgeting tips to keep you out of default on your bills.

A short sale is basically getting an agreement in place with your lender to settle your mortgage for an amount less than what you owe.

While this is not as devastating as a bankruptcy on your credit report, it does affect your credit score. A short sale will stain your credit for three years.

If one of these situations has happened to you, don’t despair. By paying your bills on time, budgeting, and keeping track of your credit utilization rate, your score will eventually improve.

How Long Does It Take To Rebuild Credit?

If you have bad credit (or lack thereof) your credit can be rebuilt. Often times when I worked in real estate the number one step for clients I worked with was to get approved for a mortgage.

Sometimes, I ran into clients that had bad credit. Some of those individuals would not be able to qualify for a mortgage.

As a result, I put them into credit repair.

As you know, there are a lot of variables that affect your credit score. The same is true for rebuilding your credit and how long it takes.

You can also follow the steps how to repair your credit yourself if you need to drastically improve your credit score to qualify for a mortgage.

If you have credit accounts that have been turned over for delinquencies to a collection agency, plan on closer to the one year period.

To rebuild credit, consistency really is the key.

You have to be able to make payments on time avoid late fees and don’t overspend or carry balances. If you’re able to achieve those tasks, you will be able to rebuild your credit sooner rather than later.

The Bottom Line On Improving Your Credit Score

This three digit number will dictate everything to you in your financial life. Knowing how to improve your credit score is a vital life lesson. If you don’t have good credit, follow the steps above to improve your credit score. There are car rental companies that don’t require a credit card so you don’t need a credit card for everything while you are rebuilding.

Rebuilding your credit may seem impossible but it can be done. Once you start following the tips and strategies mentioned above, your credit score number will be on the rise in no time.